A roof insurance claim is a formal request you submit to your homeowner's insurance company asking it to pay for roof damage caused by a covered peril under your policy. Standard HO-3 policies tie coverage to "sudden and accidental" direct physical loss from events like storms, hail, fire, or fallen trees. Gradual deterioration and aging are excluded from coverage in nearly every policy on the market. Understanding this distinction before you file saves time, money, and frustration. This guide walks you through everything from coverage basics to the step-by-step roof insurance claim process so you can act with confidence after damage occurs.

What is a roof insurance claim and what does it cover?

A roof insurance claim is your written or phone-based request for your insurer to fund repairs or full replacement after a qualifying damage event. The industry term you will see in your policy documents is a "property damage claim" filed under your homeowner's insurance policy, most commonly an HO-3 form. Both terms describe the same process, so knowing either one helps you communicate clearly with your insurer and your roofing contractor.

Covered perils under a standard homeowner's policy typically include:

- Wind and hail storms — the most common trigger for roof claims in the Southeast

- Lightning strikes — direct hits that crack decking or ignite roofing materials

- Fallen trees or limbs — sudden impact damage from a storm-toppled tree

- Fire — including wildfires and accidental house fires

- Weight of ice or snow — in regions where accumulation causes structural stress

What the policy does not cover is equally important. Insurers won't pay for a new roof simply because it is old or worn out. Moss buildup, cracked caulking around flashing, and shingles that have simply reached the end of their lifespan are maintenance issues, not insurable events. The "sudden and accidental" standard is the dividing line your adjuster will apply to every damage item on your roof.

Which roof damages are covered or excluded by typical homeowner policies?

Coverage decisions hinge on one central question: was the damage caused by a specific, sudden event or by gradual wear over time? Policies cover sudden and accidental direct physical loss but exclude normal wear and tear or maintenance neglect. That distinction sounds simple, but it creates real disputes when a storm exposes pre-existing deterioration.

Here is a practical breakdown of covered versus excluded scenarios:

Covered:

- A hailstorm dents and cracks asphalt shingles on a five-year-old GAF Timberline roof

- A pine tree falls during a thunderstorm and punctures the decking

- Wind lifts and removes a section of Owens Corning Duration shingles during a named storm

Not covered:

- Shingles that have curled, cracked, or lost granules due to age alone

- Flashing that has rusted or separated over years of thermal expansion

- Leaks caused by clogged gutters that were never cleaned

Local weather patterns matter here. Chattanooga sits in a region prone to severe spring storms, hail events, and occasional ice accumulation. That frequency of weather events means your roof takes real hits, and distinguishing storm damage from age-related wear is something a qualified inspector can document clearly.

Pro Tip: Before any storm season, schedule a professional roof inspection to establish a documented baseline condition. If a storm hits, you have proof of what was pre-existing versus what the storm caused. This single step prevents the most common adjuster disputes.

One more exclusion worth knowing: cosmetic damage. Some policies include a cosmetic damage exclusion that denies claims for dents or scuffs that do not affect the roof's function. Read your policy declarations page carefully for this language before you assume every dent is claimable.

How does the roof insurance claim process work from start to finish?

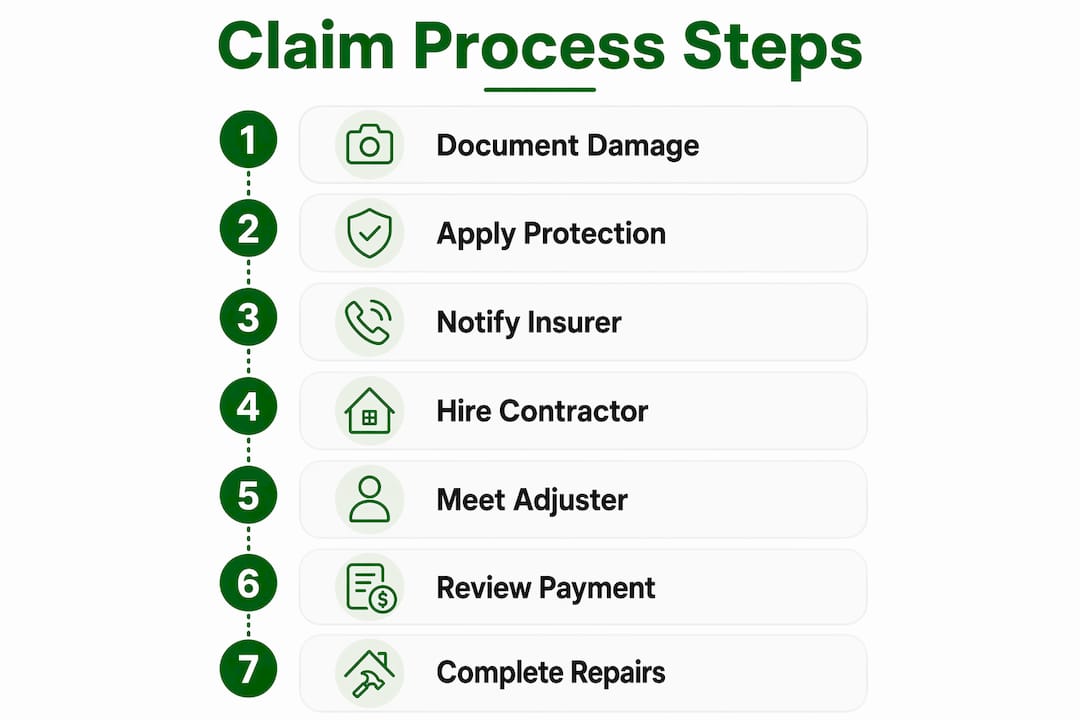

The roof insurance claim process follows a predictable sequence. Moving through it methodically protects your payout and avoids the most common reasons claims get delayed or denied.

Step 1: Document the damage immediately. Photograph and video every damaged area from the ground before anyone walks on the roof. Capture wide shots for context and close-ups for detail. Date-stamp everything using your phone's camera settings.

Step 2: Apply emergency protection. If the damage creates an opening, cover it with a tarp to prevent water intrusion. Chattanoogaroofrepairs offers same-day tarping for storm damage, which stops secondary damage that your insurer could otherwise exclude from the claim.

Step 3: Notify your insurer promptly. Call your insurance company or file online as soon as possible. Most policies require "timely notice" of a loss. Waiting weeks after a storm can give the adjuster grounds to question whether the damage is truly storm-related.

Step 4: Hire a reputable local roofing contractor for an independent inspection. A licensed contractor's written estimate gives you an independent scope of damage before the adjuster arrives. This is not optional. It is your best protection against a low initial settlement.

Step 5: Meet the adjuster on-site with your contractor present. Assembling a detailed claim packet with dated photos, a contractor scope and estimate, and any mitigation receipts helps the adjuster match the loss to specific line items. Your contractor can point out damage the adjuster might otherwise miss.

Step 6: Review the initial payment and scope of loss. With replacement cost coverage, the insurer issues an initial partial payment and holds back the depreciation amount until repairs are completed. This is called recoverable depreciation. Do not stop after the first check.

Step 7: Complete repairs and submit documentation. Once repairs are finished, submit your contractor's final invoice and any supplemental documentation. The insurer then releases the withheld depreciation. Homeowners who fail to complete repairs after receiving the initial payment forfeit that recoverable depreciation entirely.

Pro Tip: Keep a dedicated folder, physical or digital, for every document related to your claim. Include your policy declarations page, all correspondence with your insurer, contractor estimates, photos, and receipts. Adjusters and attorneys both respond faster when you can produce organized records on demand.

Common pitfalls to avoid:

- Signing any document before you understand it fully

- Accepting a verbal settlement without a written scope of loss

- Delaying repairs past your policy's repair deadline

What types of homeowner insurance policies affect roof claim payouts?

The single biggest factor in how much money you receive from a roof damage insurance claim is whether your policy pays on a Replacement Cost Value (RCV) or Actual Cash Value (ACV) basis. Policy basis is the primary factor explaining variability in claim payouts for identical damage.

| Policy Type | How payout is calculated | Impact on a 15-year-old roof |

|---|---|---|

| Replacement Cost Value (RCV) | Pays the current cost to repair or replace with like materials | Full replacement cost, minus your deductible |

| Actual Cash Value (ACV) | Pays replacement cost minus depreciation for age and condition | Significantly reduced payout; you cover the gap |

A practical example: a full shingle replacement costs $12,000. With RCV coverage and a $1,500 deductible, you receive $10,500. With ACV coverage on a 15-year-old roof that has depreciated 60%, you receive roughly $3,300 after your deductible. That $7,200 gap comes out of your pocket.

Roof age and condition directly affect ACV settlements. Insurers use depreciation schedules that reduce the value of older roofs significantly. Some insurers in high-risk states have moved to ACV-only policies for roofs over a certain age, so verifying your coverage type before a storm hits is critical.

Pro Tip: Call your insurance agent and ask one direct question: "Does my policy pay roof claims on a replacement cost or actual cash value basis?" If the answer is ACV, ask what it would cost to upgrade to RCV coverage. The annual premium difference is often far smaller than the payout difference after a major storm.

How do roofing contractors assist homeowners in the insurance claim process?

A licensed roofing contractor does far more than fix shingles during an insurance claim. The right contractor acts as your technical advocate from the first inspection through final payment.

Here is what a qualified contractor brings to your claim:

- Detailed damage assessment. A contractor trained in storm damage identifies hail strikes, wind uplift, and impact damage that untrained eyes miss. Chattanoogaroofrepairs uses a 21-point inspection process to document every damage item systematically.

- Written scope and estimate. The contractor prepares a line-item estimate that matches the format adjusters use. This makes it easier for the adjuster to approve specific repairs rather than offer a lump-sum lowball figure.

- Adjuster meeting participation. Having your contractor present when the adjuster inspects the roof means damage gets flagged in real time. Adjusters are thorough, but they are also managing dozens of claims. Your contractor's presence keeps the inspection focused.

- Supplemental claim support. If the adjuster's initial scope misses items, your contractor can prepare a supplemental claim with photos and documentation to request additional payment. This is standard practice, not confrontational.

- Material sourcing with manufacturer backing. Contractors using GAF or Owens Corning materials can offer manufacturer-backed warranties that protect your repair long after the claim closes.

Storm chasers who pressure homeowners to sign assignment of benefits documents are a serious risk after major weather events. These out-of-state contractors often charge inflated rates, perform substandard work, and leave homeowners with no recourse. Choosing a locally licensed, insured contractor protects you from this outcome.

Pro Tip: Check your contractor's license status with the Tennessee Department of Commerce and Insurance before signing anything. A legitimate local contractor will not pressure you to sign over your claim rights. Ask for proof of insurance and references from recent local jobs.

You can also review signs of storm damage on your own before calling a contractor, which helps you describe the situation accurately when you make that first call.

Key takeaways

A successful roof insurance claim depends on understanding your policy type, documenting damage thoroughly, and working with a licensed local contractor from the first inspection through final payment.

| Point | Details |

|---|---|

| Coverage requires sudden damage | Insurers cover storm, hail, fire, and fallen trees but exclude age-related wear and maintenance neglect. |

| RCV vs. ACV determines your payout | Replacement cost policies pay full repair costs; actual cash value policies deduct depreciation, often leaving a large gap. |

| Document everything before filing | Dated photos, contractor estimates, and mitigation receipts form the claim packet that drives adjuster decisions. |

| Complete repairs to recover full payment | Stopping after the first check forfeits recoverable depreciation on replacement cost policies. |

| Use a licensed local contractor | A qualified contractor documents damage, attends adjuster visits, and files supplements to protect your settlement. |

What I've learned after years of watching homeowners navigate roof claims

The homeowners who come out of the claims process feeling satisfied share one habit: they treated the claim like a project, not a phone call. They documented damage the same day it happened, called a licensed contractor before they called their insurer, and stayed involved at every step. The ones who struggled handed everything off and assumed the system would work in their favor.

The most underestimated risk I see is the assignment of benefits trap. After a major storm rolls through Chattanooga, out-of-state contractors flood the area with door-to-door offers to "handle everything." Signing that document transfers your claim rights to the contractor. You lose control of the scope, the timeline, and the quality of work. I have seen homeowners end up with a finished roof and a lawsuit from a contractor disputing the settlement amount.

Understanding your policy before storm season is the move most homeowners skip. Knowing whether you have RCV or ACV coverage, what your deductible is, and whether you have a cosmetic damage exclusion takes 15 minutes with your declarations page. That 15 minutes can be worth thousands of dollars when a claim is filed. Local resources like Chattanoogaroofrepairs offer free, no-pressure inspections that give you a clear picture of your roof's current condition, which is exactly the kind of baseline documentation that protects you when you file.

— Steve

How Chattanoogaroofrepairs supports your roof insurance claim

When storm damage hits your home, you need a local team that knows the claims process as well as they know roofing.

Chattanoogaroofrepairs provides storm and hail damage repair across Chattanooga and surrounding areas, backed by certified expertise with GAF and Owens Corning materials. From same-day tarping to 21-point inspections and full residential roofing services, the team supports every stage of your claim with detailed documentation, adjuster meeting participation, and transparent pricing. Contact Chattanoogaroofrepairs today for a free, no-pressure estimate and get the local expertise your claim deserves.

FAQ

What is a roof insurance claim in simple terms?

A roof insurance claim is a formal request to your homeowner's insurance company to pay for roof damage caused by a covered event like a storm, hail, or fallen tree. It is filed under your homeowner's policy and triggers an adjuster inspection to assess the damage and determine your payout.

What does homeowner's insurance typically cover for roof damage?

Standard homeowner's policies cover sudden and accidental damage from wind, hail, lightning, fire, and fallen trees. Gradual wear, aging, and maintenance neglect are excluded from coverage under nearly all policies.

How do I file a homeowner insurance roof claim?

Document the damage with photos, apply emergency protection like a tarp, then notify your insurer promptly. Hire a licensed local contractor for an independent inspection before the adjuster visits to protect your settlement.

What is the difference between RCV and ACV for a roof claim?

Replacement Cost Value (RCV) pays the current cost to repair or replace your roof, while Actual Cash Value (ACV) deducts depreciation based on your roof's age and condition. On an older roof, the ACV payout can be dramatically lower than the actual repair cost.

Can a roofing contractor help with my insurance claim?

Yes. A licensed contractor documents damage, prepares a line-item estimate, attends the adjuster inspection, and files supplemental claims if the initial scope is incomplete. Choosing a locally licensed contractor protects you from out-of-state storm chasers who may pressure you to sign over your claim rights.