Roofing insurance coverage is the protection your standard homeowners insurance policy provides against sudden, accidental roof damage caused by specific named perils. Under a typical HO-3 policy, covered named perils include wind, hail, fire, lightning, and falling objects. What roofing insurance covers does not extend to gradual wear, maintenance neglect, or pre-existing damage. Your payout depends on whether your policy uses Replacement Cost Value (RCV) or Actual Cash Value (ACV), a distinction that can mean thousands of dollars in the difference. Knowing these details before you file a claim protects your wallet and your home.

What does roofing insurance coverage include for common damage events?

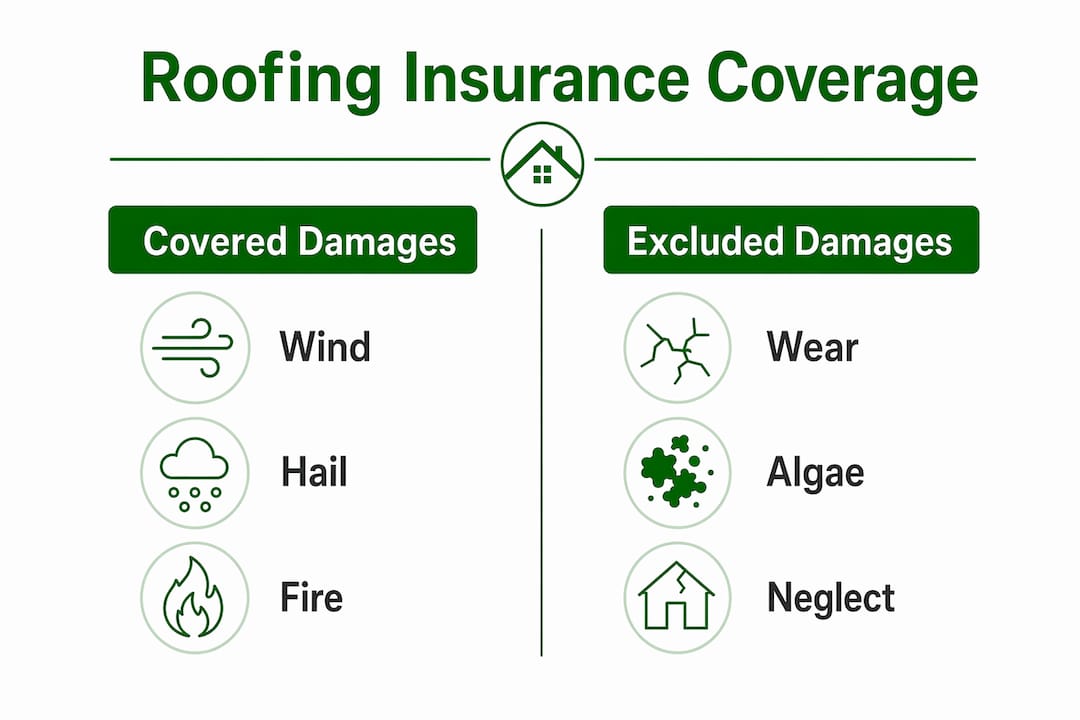

Standard homeowners insurance covers roof damage that is sudden and accidental. The damage must result from a named peril listed in your policy. Gradual deterioration does not qualify, no matter how severe it looks.

The most common covered perils are:

- Wind damage: Shingles torn off or lifted by high winds, including damage from hurricanes and severe thunderstorms

- Hail damage: Dents, cracks, or granule loss on shingles that compromise their protective function

- Fire and lightning: Direct fire damage or burns caused by a lightning strike

- Falling objects: Tree limbs, branches, or debris that strike the roof during a storm

- Sudden water intrusion: Water damage that enters through a storm-created breach, not through a slow leak

Wind and hail claims occur at a rate of 2.80 per 100 insured homes annually. That figure makes wind and hail the single most frequent source of roofing insurance claims in the country.

What roofing insurance covers does not include age-related decline, moss or algae buildup, or damage caused by skipping routine maintenance. Cosmetic damage only, such as minor surface scuffs with no effect on shingle function, is also frequently excluded or disputed. Insurers draw a clear line between damage that compromises your roof's ability to protect your home and damage that only affects appearance.

Pro Tip: Take photos of your roof at least once a year when no damage is present. A dated baseline photo set makes it far easier to prove that storm damage is new and not pre-existing.

How do RCV and ACV payouts differ for roof claims?

The financial mechanics of a roofing insurance claim depend almost entirely on your payout type. RCV and ACV policies produce very different results, especially on older roofs.

| Factor | Replacement Cost Value (RCV) | Actual Cash Value (ACV) |

|---|---|---|

| What it pays | Full repair or replacement cost | Repair cost minus depreciation |

| Depreciation applied | No | Yes, based on roof age |

| Example: $18,000 roof | Pays $18,000 minus deductible | May pay $9,000 or less |

| Best for | Newer roofs | Older roofs with limited coverage |

| Premium cost | Higher | Lower |

On an $18,000 roof replacement, an RCV policy pays the full amount minus your deductible. An ACV policy deducts years of depreciation first, which can cut your payout in half on a roof that is 10 or more years old.

Deductibles add another layer of complexity. Wind and hail deductibles are often percentage-based rather than flat dollar amounts. A 2% deductible on a $300,000 home means you pay $6,000 out of pocket before insurance covers anything. That is a very different number than a flat $1,000 deductible.

RCV policies also include a depreciation holdback. Insurers withhold depreciation funds until you submit proof that repairs are complete. You must finance the initial repair cost yourself, then submit the final invoice to recover the withheld amount. Plan for this cash flow gap before you sign a contract with a roofing contractor.

Pro Tip: Read your declarations page carefully before storm season. Confirm whether your roof is covered under RCV or ACV, and check whether your wind and hail deductible is a flat amount or a percentage of your home's insured value.

How to file a roofing insurance claim effectively

Filing a roofing insurance claim successfully depends on preparation, timing, and the quality of your documentation. A claim's outcome is largely determined before the adjuster ever sets foot on your property.

Follow these steps to give your claim the best chance of approval:

- Document damage immediately. Photograph every affected area from multiple angles within 24 hours of the storm. Include close-ups of damaged shingles, dents, and any interior water intrusion.

- Schedule a professional roof assessment. Qualified contractor assessments are critical for distinguishing sudden storm damage from pre-existing wear. An adjuster will look for the same distinction.

- Install temporary protection. A tarp or emergency cover stops further water damage and preserves your claim's validity. Learn more about why temporary repairs matter before the adjuster arrives.

- Submit your claim promptly. Most policies require you to report damage within a specific window. Delays can give insurers grounds to question whether the damage is storm-related.

- Review the adjuster's report. Compare it against your contractor's written assessment. Discrepancies in scope or damage classification are common and worth disputing.

One critical judgment call: filing a claim is not always beneficial if the repair cost falls below your deductible. A claim on record can raise your future premiums or complicate coverage renewals, even if you receive no payout. Do the math before you call your insurer.

When adjusters deny claims for cosmetic hail damage, a contractor who can document functional compromise in writing gives you a strong basis for appeal. Cosmetic damage that accelerates shingle degradation or allows water infiltration is functional damage by any reasonable standard. The right contractor knows how to make that case.

For a detailed walkthrough of the full process, the roof insurance claim guide from Chattanoogaroofrepairs covers documentation, timelines, and what to expect from your insurer.

How roof age and upgrades affect your insurance coverage

Your roof's age and condition directly affect what coverage your insurer will offer. Insurance companies inspect roofs at policy issuance and renewal. A roof in poor condition can trigger a switch from RCV to ACV coverage, or result in a denial of coverage entirely.

Here is what affects your roofing insurance policy details most:

- Roof age: Most insurers apply depreciation aggressively on roofs older than 15–20 years. Some carriers refuse to write RCV policies on roofs past a certain age threshold.

- Roofing material: Impact-resistant shingles rated Class 3 or Class 4 by UL 2218 qualify for premium discounts in many states. Metal roofing and GAF or Owens Corning architectural shingles often meet or exceed insurer standards for durability.

- FORTIFIED roof certification: Homeowners who upgrade to a certified FORTIFIED roof system see average premium savings of 22%, with median annual premiums dropping from $5,625 to $4,375. That is a real, measurable return on a roofing investment.

- Regional storm risk: Homes in high-risk zones like Chattanooga, Tennessee face more frequent hail and wind events. Insurers in these areas scrutinize roof condition more closely at renewal.

- Maintenance record: A roof with documented annual inspections signals to insurers that you are a low-risk policyholder. No documentation signals the opposite.

Newer roofs and impact-resistant materials can significantly improve your insurance eligibility and lower your premiums, especially in storm-prone regions. If your roof is approaching 15 years old, a proactive inspection and upgrade plan is worth more than waiting for the next storm to force the issue.

Key takeaways

Roofing insurance coverage pays for sudden, accidental damage from named perils, and your payout type, deductible structure, and roof condition determine exactly how much you receive.

| Point | Details |

|---|---|

| Named perils only | Coverage applies to wind, hail, fire, lightning, and falling objects, not wear or neglect. |

| RCV vs. ACV matters | RCV pays full replacement cost; ACV deducts depreciation, which can cut payouts significantly on older roofs. |

| Deductibles can be percentage-based | A 2% wind and hail deductible on a $300,000 home means $6,000 out of pocket before insurance pays. |

| Document damage immediately | Dated photos and a contractor's written assessment are the two strongest tools for claim approval. |

| Upgrades reduce premiums | FORTIFIED roof certification saves an average of 22% on annual premiums, with median savings near $1,250 per year. |

My take on navigating roofing insurance claims

Working with homeowners through the claims process has taught me one consistent lesson: the gap between what insurance should pay and what it actually pays almost always comes down to documentation quality.

Adjusters are not adversaries, but they are working from a checklist. If your damage looks like it could be old, they will treat it as old. A contractor who shows up with a written assessment, dated photos, and specific references to storm-related failure patterns changes that conversation entirely. That is not salesmanship. That is advocacy.

I have also seen homeowners file claims they should not have filed. A $1,500 repair on a policy with a $2,000 deductible produces no payout and a claim on your record. That record can cost you more in premium increases over three years than the repair itself. The math matters.

The depreciation holdback catches people off guard more than almost anything else. You get an initial check, you hire a contractor, and then you wait for the insurer to release the withheld depreciation after the work is verified. If you did not budget for that gap, you may find yourself short on funds mid-project. Ask your contractor and your insurer to walk you through the payment timeline before work begins.

The homeowners who come out ahead are the ones who treat their roof as a documented asset, not just a structure overhead. Annual inspections, good records, and a contractor who understands the insurance process are worth more than any single claim.

— Steve

How Chattanoogaroofrepairs helps you get the most from your coverage

When storm damage hits, the speed and quality of your response determines your claim outcome. Chattanoogaroofrepairs provides certified roof inspections, same-day tarping, and detailed written assessments that give your insurer exactly what it needs to process your claim.

Our team works with GAF and Owens Corning materials and carries out comprehensive 21-point inspections before and after every storm event. We handle storm and hail damage repairs across Chattanooga and the surrounding area, and we know how to document damage in the language insurers respond to. Whether you need a roof leak repair or a full replacement, we provide transparent pricing and no-pressure guidance from the first call. Contact Chattanoogaroofrepairs today for a free roof inspection and claim consultation.

FAQ

What perils does standard roofing insurance cover?

Standard homeowners insurance covers roof damage from wind, hail, fire, lightning, and falling objects under named peril policies. Gradual wear, maintenance neglect, and pre-existing damage are excluded.

What is the difference between RCV and ACV for roof claims?

RCV pays the full cost to repair or replace your roof minus your deductible, while ACV deducts depreciation based on your roof's age before paying out. On an older roof, ACV can reduce your payout by 50% or more.

Should I always file a claim for roof damage?

Not always. If the repair cost is lower than your deductible, filing a claim produces no payout and adds a claim to your record, which can raise future premiums. Calculate the full cost before contacting your insurer.

How does roof age affect my insurance coverage?

Insurers may switch older roofs from RCV to ACV coverage or deny coverage entirely based on condition found during policy inspections. Roofs older than 15–20 years face the greatest risk of coverage limitations.

Can a roofing contractor help with my insurance claim?

A qualified contractor can document the sudden nature of damage, differentiate it from pre-existing wear, and provide written assessments that support denied claim appeals, particularly for cosmetic hail damage disputes.