Roof condition is a primary factor insurers use to calculate business property insurance premiums, coverage terms, and claim payouts. A commercial roof's age, material type, maintenance history, and current damage status all feed directly into an insurer's risk assessment. Neglected or aging roofs trigger higher premiums, coverage restrictions, and outright claim denials. Business owners and property managers who understand how roof condition affects business insurance can take concrete steps to protect their coverage and reduce costs before a storm or inspection forces the issue.

How roof condition affects business insurance premiums

Insurers treat your roof as the single most visible indicator of property risk. A well-maintained roof signals responsible ownership. A deteriorating one signals future claims.

The two most critical variables are age and material. Most commercial insurance carriers switch roof settlements from replacement cost value (RCV) to actual cash value (ACV) once a roof reaches 15–20 years old. That shift alone can cut a claim payout by 50%–70%. A $90,000 RCV claim can settle for under $45,000 after depreciation is applied through a roof age endorsement.

Material type compounds the age factor. Metal roofs carry useful lifespans of 40–70 years and depreciate slowly. Three-tab asphalt shingles typically last 15–20 years and depreciate faster. Insurers assign different depreciation schedules to each material, which directly affects how much you receive after a loss.

Here is what insurers typically evaluate during underwriting:

- Roof age: Roofs older than 15–20 years often trigger ACV-only settlements or coverage non-renewal.

- Material type: Metal, tile, and impact-resistant shingles like GAF Timberline HDZ earn lower risk ratings than standard asphalt.

- Installation quality: Improper flashing or poor workmanship raises the probability of water intrusion claims.

- Maintenance history: Documented repairs and inspections signal low risk. No records signal the opposite.

- Current damage: Visible deterioration, missing shingles, or active leaks can result in policy non-renewal at the next audit.

Pro Tip: Ask your insurer specifically whether your policy contains a roof age endorsement. Many owners overlook these endorsements at renewal, then discover their payout is half what they expected after a major loss.

Does proactive roof maintenance lower your insurance costs?

Preventative maintenance is the most underused tool business owners have for controlling insurance costs. Regular upkeep reduces the frequency and severity of claims, which directly lowers your risk profile.

Investing $2,000–$3,000 annually on preventative maintenance for a 20,000 sq. ft. commercial roof can help avoid $100,000–$200,000 in reactive repair and secondary damage costs. That math is hard to argue with. Proactive maintenance saves approximately $0.11 per square foot annually compared to reactive costs.

A documented maintenance program also gives you negotiating power at renewal. Providing maintenance records to your insurer, including inspection reports, drain cleaning logs, and repair receipts, is a recognized tool for preventing non-renewal and securing broader coverage terms.

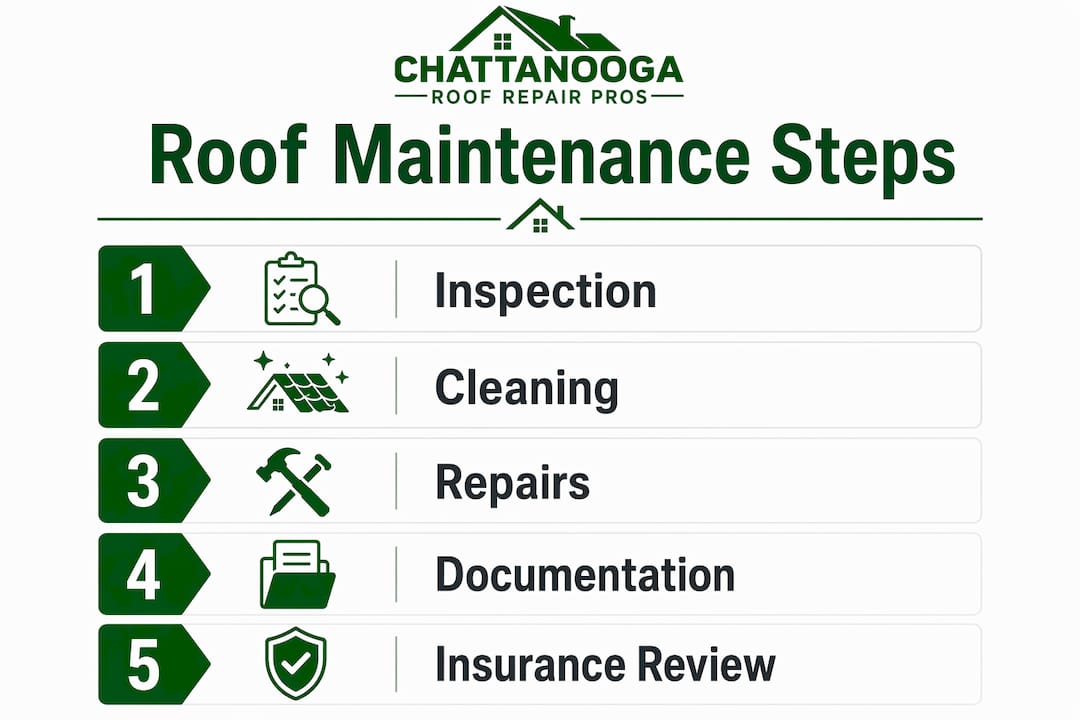

Follow these four steps to build a maintenance record that insurers respect:

- Schedule professional inspections twice a year. Spring and fall inspections catch damage from winter ice and summer heat before it worsens. Use a licensed contractor who provides a written report.

- Clean gutters and drains after every major storm. Clogged drains are classified as a maintenance failure by most carriers. Insurers deny claims tied to water backup from blocked drainage.

- Repair minor damage within 30 days of discovery. Document every repair with photos, invoices, and the contractor's name. This creates a timeline that separates old damage from new storm damage.

- Archive all records in a single, dated file. A comprehensive maintenance portfolio is an asset during claims adjustment. It proves roof integrity and responsible stewardship, which reduces claim disputes and improves settlement outcomes.

Pro Tip: Pair your maintenance log with before-and-after photos for every repair. This documentation is your strongest defense if an insurer tries to classify new storm damage as pre-existing wear and tear.

How roof damage and delayed repairs lead to claim denials

Claim denials tied to roof damage almost always come down to one of two causes: gradual neglect or delayed mitigation. Understanding both protects your coverage.

Insurers distinguish sharply between sudden storm damage and gradual wear. Damage from neglected flashing or clogged drains is classified as wear and tear, a standard policy exclusion. If your roof has been leaking for months and a storm worsens the damage, the carrier will argue the underlying cause was maintenance failure, not the storm. That argument often wins.

The second denial trigger is delayed mitigation. Emergency weatherproofing within 24–48 hours is a standard insurer requirement. Delays beyond 72 hours often cause partial or complete denial of secondary damage claims. Mold growth, interior collapse, and inventory loss that follow a roof breach are all considered preventable if you act quickly. Insurers will not pay for damage they consider avoidable.

Liability risk extends beyond the insurance claim itself. Undisclosed leaks or roof hazards can expose property owners to personal or corporate liability for injuries. If a contractor or employee is injured because of a known roof hazard you failed to address, the risk shifts from your insurer to you directly. That exposure can far exceed any single insurance claim.

Key denial triggers to watch for:

- Leaks left unrepaired for more than 48–72 hours after discovery

- Missing or damaged flashing attributed to long-term neglect

- Clogged roof drains causing water backup and interior damage

- No documentation of prior inspections or repairs

- Failure to install emergency tarping after storm damage

For guidance on filing a roof damage claim correctly, including how to separate maintenance issues from storm damage, the process matters as much as the repair itself.

RCV vs. ACV: How insurers calculate your roof claim payout

Replacement cost value (RCV) and actual cash value (ACV) are the two settlement methods insurers use for roof claims. The difference between them can be tens of thousands of dollars.

RCV pays the full cost to replace your roof with a comparable new one, regardless of the old roof's age. ACV pays RCV minus depreciation. The older and more deteriorated your roof, the greater the depreciation deduction and the smaller your check.

Condition-based inspections score roofs on a scale of 1 to 5 to adjust depreciation and determine ACV settlement amounts. A roof scored poorly due to granule loss, cracking, or ponding water will receive a steeper depreciation deduction than straight-line age calculations alone would produce. This scoring system can result in more severe payout reductions than many owners anticipate.

| Settlement Method | How it works | Impact on payout |

|---|---|---|

| Replacement cost value (RCV) | Pays full replacement cost, no depreciation deducted | Highest payout; applies to newer, well-maintained roofs |

| Actual cash value (ACV) | Pays replacement cost minus depreciation | Reduced payout; triggered by age or condition endorsements |

| Condition-based ACV | Depreciation set by inspection score, not just age | Can produce steeper reductions than standard ACV |

Insurance carriers switch coverage from RCV to ACV through endorsements embedded in the policy, often without clear notice to the owner. These endorsements frequently activate at renewal once a roof crosses a defined age threshold. Auditing your policy documents every year is the only reliable way to catch this shift before a claim.

Practical steps to protect your coverage and reduce premiums

Business owners who treat roof condition as an insurance asset, not just a maintenance task, consistently get better outcomes at renewal and after claims. The steps below are concrete and repeatable.

- Get a professional inspection annually. A written report from a licensed contractor gives you documented proof of roof condition. Chattanoogaroofrepairs provides comprehensive 21-point inspections that produce the kind of detailed records insurers want to see.

- Document every repair with photos and invoices. Follow the best practices for roof documentation to build a file that clearly separates pre-existing conditions from new storm damage.

- Notify your insurer within 24 hours of any damage. Prompt notification starts the claims clock and establishes that you acted responsibly. Pair notification with emergency tarping or other mitigation to protect your secondary damage coverage.

- Audit your policy for roof endorsements every year. Look specifically for age-based or condition-based endorsements that switch your settlement from RCV to ACV. If you find one, ask your broker whether a roof upgrade or inspection report can remove it.

- Keep a property damage documentation system. Property managers handling multiple buildings benefit from a centralized log. The same principles that apply to glass damage documentation apply directly to roof records: dates, photos, contractor names, and repair costs all matter.

Pro Tip: If your insurer denies a claim by conflating old wear with new storm damage, a thorough maintenance record is your strongest rebuttal. The primary dispute in many claim denials is cause of loss, and documentation forces carriers to separate the two.

Key Takeaways

A commercial roof's age, material, and maintenance record directly determine whether your insurer pays full replacement cost or a sharply depreciated amount after a loss.

| Point | Details |

|---|---|

| Age triggers ACV settlements | Roofs aged 15–20 years often shift from RCV to ACV, cutting payouts by 50%–70%. |

| Maintenance saves money | Spending $2,000–$3,000 annually on upkeep can prevent $100,000–$200,000 in reactive repair costs. |

| Delayed mitigation voids coverage | Failing to act within 48–72 hours after damage can result in denial of secondary damage claims. |

| Policy endorsements reduce payouts | Age and condition endorsements often activate at renewal without clear notice to the owner. |

| Documentation wins disputes | Inspection reports, photos, and repair receipts separate storm damage from wear and tear during claims. |

What I've learned after years of watching business owners lose claims they should have won

Most business owners I talk to are surprised when their claim settles for half the expected amount. They assumed their policy covered full replacement. What they missed was a single endorsement buried in the renewal documents that switched their roof settlement to ACV the moment the roof turned 15.

The documentation gap is the other pattern I see constantly. A storm hits, the owner files a claim, and the adjuster points to granule loss and cracked flashing as evidence of pre-existing neglect. Without a maintenance record, the owner has no way to prove those conditions developed after the storm. The insurer wins by default.

The owners who come out ahead are the ones who treat their roof like a financial asset. They schedule inspections, keep records, and act within hours after a storm. When a claim comes in, they hand the adjuster a folder with dated photos, repair invoices, and inspection reports going back three years. Adjusters have very little room to deny a claim that is that well documented.

Emergency response is the piece most people underestimate. Getting a tarp on a damaged roof within 24 hours is not just good practice. It is a contractual obligation in most commercial policies. Skipping it can void coverage for every dollar of interior damage that follows. That is a risk no business can afford.

— Steve

Chattanoogaroofrepairs: Roof services built for insurance outcomes

Business owners in Chattanooga need a roofing partner who understands the insurance side of the work, not just the repair side. Chattanoogaroofrepairs provides professional inspections, documented repairs, and emergency response services designed to support your coverage from the ground up.

Our comprehensive roofing services include 21-point inspections that produce the detailed written reports insurers require, same-day emergency tarping to protect your secondary damage coverage, and roof leak repair backed by GAF and Owens Corning materials. Every job comes with transparent pricing, full documentation, and no-pressure guidance on your next steps. When your insurer asks for proof of maintenance or mitigation, we make sure you have it.

FAQ

How does roof age affect business insurance premiums?

Roofs aged 15–20 years often trigger a policy switch from replacement cost value to actual cash value, which can reduce claim payouts by 50%–70%. Older roofs also increase the likelihood of premium hikes or non-renewal at the next policy audit.

What happens if I don't repair roof damage quickly?

Insurers require emergency mitigation within 24–48 hours of damage discovery. Delays beyond 72 hours frequently result in denial of secondary damage claims, including mold, interior collapse, and inventory loss.

Can roof maintenance actually lower my insurance premiums?

Yes. A documented maintenance history is a recognized negotiation tool at renewal. Carriers view inspection reports, drain cleaning logs, and repair receipts as evidence of low risk, which can prevent non-renewal and support broader coverage terms.

What is the difference between RCV and ACV for roof claims?

Replacement cost value (RCV) pays the full cost to replace your roof. Actual cash value (ACV) deducts depreciation based on age and condition. The older or more deteriorated your roof, the larger the deduction and the smaller your settlement check.

Does roof damage affect my liability coverage too?

Yes. Known roof hazards that go unaddressed can shift liability from your insurer to you personally. If a contractor or employee is injured because of an undisclosed roof defect, you may face personal or corporate liability beyond what your property insurance covers.