A roof repair seller concession is a negotiated credit applied at closing that reduces a buyer's cash-to-close requirement instead of requiring the seller to manage repairs directly. This approach has become the preferred path in most real estate transactions because it gives buyers control over repair quality and timing. Knowing how to request roof repair seller concession credits correctly, with the right documentation and an understanding of lender limits, separates buyers who close confidently from those who lose deals over roof disputes. FHA, VA, and conventional loan programs each set different caps on how much sellers can contribute, which makes understanding those rules a non-negotiable first step.

What seller concessions for roof repair are and how they work at closing

A seller concession is a dollar amount the seller agrees to credit toward the buyer's costs at closing. Repair credits reduce the buyer's cash-to-close rather than delivering direct cash to the buyer. The credit appears on the settlement statement as a line item, offsetting allowable closing expenses. That distinction matters because buyers cannot pocket the difference as cash.

Lenders treat these credits carefully. Most lenders prefer repair credits labeled as closing cost credits rather than "repair allowances" to avoid triggering additional inspections that delay closing. The label on the contract amendment affects how underwriters review the file. A well-drafted amendment names the credit amount and ties it specifically to the roof repair scope identified in the inspection report.

Seller concession limits are capped by loan type and down payment level. The table below shows standard limits:

| Loan Type | Down Payment | Maximum Seller Concession |

|---|---|---|

| FHA | Any | Up to 6% of purchase price |

| VA | Any | Up to 4% of purchase price |

| Conventional | Less than 10% | Up to 3% of purchase price |

| Conventional | 10%–25% | Up to 6% of purchase price |

| Conventional | Over 25% | Up to 9% of purchase price |

| Investment property | Any | Up to 2% of purchase price |

These caps apply to all seller contributions combined, not just roof repair credits. A buyer using an FHA loan on a $300,000 home can receive a maximum of $18,000 in total seller concessions. If closing costs already consume $10,000 of that cap, only $8,000 remains available for a roof repair credit.

Key points buyers should confirm before submitting a concession request:

- Verify total seller concessions already negotiated in the purchase contract

- Confirm the remaining concession capacity with your lender before requesting a roof credit

- Ask your lender whether the credit must be labeled as a closing cost credit or repair allowance

- Get the agreed credit amount written into a signed contract amendment before closing

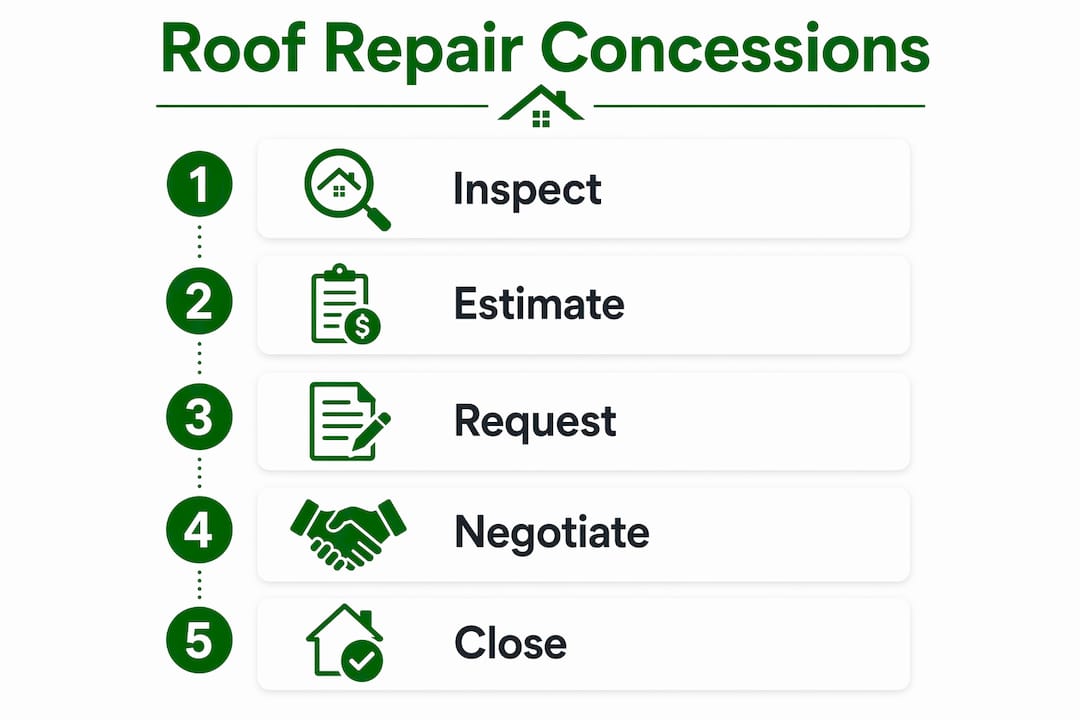

How to document and justify your roof repair concession request

Documentation is the single most important factor in a successful roof repair negotiation. Written, itemized bids from licensed roofing contractors carry far more negotiation weight than vague estimates or verbal quotes. A seller's agent will challenge any number that lacks a professional signature and line-item breakdown.

The strongest requests follow a clear sequence:

- Order a home inspection first. The inspection report is your foundation. It identifies specific roof defects with photos, measurements, and condition ratings.

- Obtain at least two written bids from licensed contractors. Each bid should itemize labor, materials, and any code-compliance upgrades required.

- Cross-reference bids with the inspection findings. Your request should address only the defects the inspector flagged, not a wish list of upgrades.

- Review roof replacement cost disclosures relevant to your market. Regional material and labor costs vary significantly and affect what a reasonable credit looks like.

- Submit the request in writing with all supporting documents attached. Include the inspection report, both contractor bids, and a cover letter summarizing the safety and livability concerns.

- Time the request correctly. Submit after the inspection period opens but with enough time before the closing date to allow for negotiation and lender review.

Focus your request on defects that affect safety, functionality, or structural integrity. Prioritizing repairs that affect safety and value rather than cosmetic issues leads to more productive negotiations. A seller is far more likely to agree to a credit for active leaks or deteriorated flashing than for faded shingles.

Pro Tip: Add a 10–15% buffer to your contractor estimates when calculating the credit amount you request. Roof repairs frequently uncover hidden damage once work begins, and the credit agreement is typically final. You cannot ask for more money after closing.

Negotiation strategies for requesting roof repair seller concessions

The most effective strategy in roof repair negotiation is requesting a credit rather than asking the seller to complete repairs before closing. Sellers prefer financial credits over direct repairs because credits simplify the transaction and reduce the risk of closing delays from repair coordination. Buyers benefit because they control which contractor does the work and can verify quality after moving in.

Market conditions shape how much leverage you have. In a buyer's market or a balanced market, sellers expect concession requests and budget for them. In a competitive seller's market, an aggressive repair request can kill a deal. Read the market before deciding how hard to push.

The table below compares common negotiation approaches and their typical outcomes:

| Approach | Best Market Condition | Typical Outcome |

|---|---|---|

| Request closing cost credit | Any market | Clean, fast resolution; lender-friendly |

| Request seller-performed repairs | Buyer's market | Slower closing; quality risk for buyer |

| Request price reduction | Buyer's or balanced market | Reduces purchase price; affects appraisal |

| Escrow holdback | Lender-dependent | Funds held until repairs verified post-closing |

| Walk away from deal | Any market | Protects buyer; loses property |

Frame your request as a practical solution, not an accusation. Language like "we'd like a credit to address the roof issues identified in the inspection" lands better than "the roof is failing and we need $15,000." Sellers respond to tone. A collaborative approach keeps deals alive.

Additional tactics worth knowing:

- Offer to split the credit amount if the seller pushes back, rather than holding firm on the full number

- Accept a price reduction as an alternative when the concession cap is already maxed out

- Ask about why roof repairs speed up closings to frame the conversation around mutual benefit

- Confirm that effective negotiation balances firmness on safety defects with flexibility in competitive markets

When do lenders require physical repairs instead of concessions?

Lenders do not always accept a credit as a substitute for actual repairs. FHA and VA appraisals follow strict minimum property standards, and a roof in poor condition can trigger mandatory repair requirements before the loan closes.

Certain roof defects with less than two years of remaining life may trigger mandatory physical repairs before closing rather than qualifying for concession credits. This is a critical distinction. If the appraiser flags the roof as a safety or habitability concern, the lender will condition loan approval on completed repairs, not a credit.

A roof that an FHA or VA appraiser deems unsafe or structurally compromised cannot be addressed with a closing cost credit alone. The lender will require documented proof of completed repairs before funding the loan, which means the seller must act or the deal must restructure entirely.

Conditions that commonly trigger mandatory repairs rather than credits include:

- Active leaks that have caused interior water damage

- Missing or severely deteriorated shingles exposing the roof deck

- Sagging or structurally compromised roof sections

- Evidence of mold or rot tied directly to roof failure

- Appraiser notation of less than two years of remaining roof life

Conventional loans follow Fannie Mae and Freddie Mac guidelines, which are less prescriptive than FHA or VA standards but still require the property to be safe and habitable. Buyers using conventional financing have more flexibility to negotiate credits for moderate roof issues. Buyers using government-backed loans should review signs that indicate replacement before submitting a concession request, since a replacement-level roof may trigger appraisal conditions regardless of loan type.

Interior moisture damage linked to roof failure can also affect adjacent systems. Buyers should check whether moisture damage to window frames or other interior components requires separate repair requests, since lenders may flag those independently.

Common pitfalls to avoid when requesting roof repair concessions

The most common mistake buyers make is overreaching. Requesting credits for minor cosmetic issues alongside legitimate structural defects weakens the entire request. Sellers and their agents dismiss inflated lists, and the negotiation stalls.

Buyers cannot ask for more money after closing if actual repair costs exceed the negotiated credit. That finality means your estimate must be thorough before you sign the amendment. Use the 10–15% buffer mentioned earlier and get your bids from licensed contractors who have reviewed the actual roof, not just the inspection report.

Pro Tip: Verify that the total credit amount, combined with all other seller concessions, stays within your lender's allowed cap before signing the amendment. A credit that exceeds the cap will be reduced at closing, leaving you short on funds.

Avoid these additional mistakes:

- Submitting a concession request without attaching the inspection report and contractor bids

- Using round numbers without itemized support (a request for exactly $10,000 with no backup raises red flags)

- Delaying the request until the final week before closing, leaving no time for negotiation

- Failing to specify in the amendment what the credit covers, which creates disputes at closing

- Skipping a review of honest roofing estimate practices before accepting a contractor's bid as your negotiation anchor

Work closely with your real estate agent throughout the process. A good agent knows the seller's situation, the local market, and how to frame requests in writing. A good roofing contractor provides the documentation that makes the request credible.

Key Takeaways

A successful roof repair seller concession request depends on accurate documentation, lender-compliant credit amounts, and a negotiation tone that keeps the deal moving forward.

| Point | Details |

|---|---|

| Credits reduce cash-to-close | Seller concessions lower what you pay at closing, not direct cash in hand. |

| Lender caps vary by loan type | FHA allows up to 6%, VA up to 4%, and conventional loans range from 3–9% based on down payment. |

| Documentation wins negotiations | Itemized bids from licensed contractors are the strongest support for any concession request. |

| Mandatory repairs override credits | FHA and VA appraisers can require physical repairs when a roof has less than two years of life remaining. |

| Credits are final at closing | Build a 10–15% buffer into your estimate because you cannot renegotiate after the deal closes. |

What I've learned from watching roof concession negotiations go wrong

I've seen buyers lose deals and buyers leave money on the table, and the pattern is almost always the same. The buyers who lose deals push too hard on cosmetic issues or submit vague requests without contractor bids. The buyers who leave money on the table accept a seller's first counteroffer without understanding what the inspection actually documented.

The most underrated move in roof repair negotiation is controlling the repair yourself. When you take a credit instead of asking the seller to fix the roof, you choose the contractor, you set the schedule, and you verify the work. Sellers often hire the cheapest contractor available to satisfy a repair requirement before closing. That rarely produces quality work. A credit puts that decision in your hands.

One thing I'd caution against is treating every roof issue as a deal-breaker. A 15-year-old roof with minor granule loss is not the same as a roof with active leaks and rotted decking. Know the difference before you negotiate. The inspection report tells you what you're actually dealing with. Let that document lead the conversation, not your anxiety about what a new roof might cost.

The buyers I've seen succeed are the ones who come to the table with two contractor bids, a clear credit amount tied to specific inspection findings, and a tone that says "let's solve this together." That combination closes deals.

— Steve

Chattanoogaroofrepairs: your partner for post-closing roof repairs

Once your concession credit is secured and you close on your new home, the real work begins. Getting the right contractor to complete the repairs correctly is just as important as negotiating the credit itself.

Chattanoogaroofrepairs serves homeowners throughout Chattanooga and the surrounding area with licensed, insured roof repair and replacement services. Whether your negotiated credit covers a targeted roof leak repair or a full roofing service and replacement, the team brings transparent pricing, GAF and Owens Corning materials, and a 21-point inspection process to every job. Same-day tarping is available for storm-related emergencies. Call Chattanoogaroofrepairs for a no-pressure estimate and put your concession credit to work on quality repairs that last.

FAQ

What is a roof repair seller concession?

A roof repair seller concession is a credit the seller agrees to apply at closing to offset the buyer's costs related to roof repairs. The credit reduces the buyer's cash-to-close rather than requiring the seller to complete repairs before closing.

How much can a seller concede for roof repairs?

The maximum depends on loan type. FHA loans allow up to 6% of the purchase price, VA loans allow up to 4%, and conventional loans allow 3–9% depending on the down payment. All seller concessions combined must stay within these caps.

Can I request a roof concession after the inspection?

Yes. The inspection report is the standard trigger for a seller repair request. Submit your request with itemized contractor bids during the inspection contingency period to allow time for negotiation before closing.

What happens if roof repair costs exceed my concession credit?

The buyer absorbs the difference. Credit agreements are final at closing, so build a 10–15% buffer into your estimate to cover unexpected costs uncovered during the repair.

Do FHA loans require physical roof repairs instead of credits?

FHA appraisers can require physical repairs when a roof has less than two years of remaining life or poses a safety or habitability concern. In those cases, a closing cost credit alone will not satisfy the lender's conditions.