A storm damage supplement is a formal request to your insurance company for additional payment when the initial claim estimate is incomplete or undervalued. In the roofing industry, this process is known more precisely as a supplemental insurance claim. Understanding what a storm damage supplement is gives you the power to recover the full cost of repairs rather than accepting a payout that falls short. Replacement Cost Value, or RCV, is the standard insurance measure for what it costs to fully restore your property. Supplements exist to close the gap between what the adjuster first estimated and what the repairs actually require.

What is a storm damage supplement and how does it work?

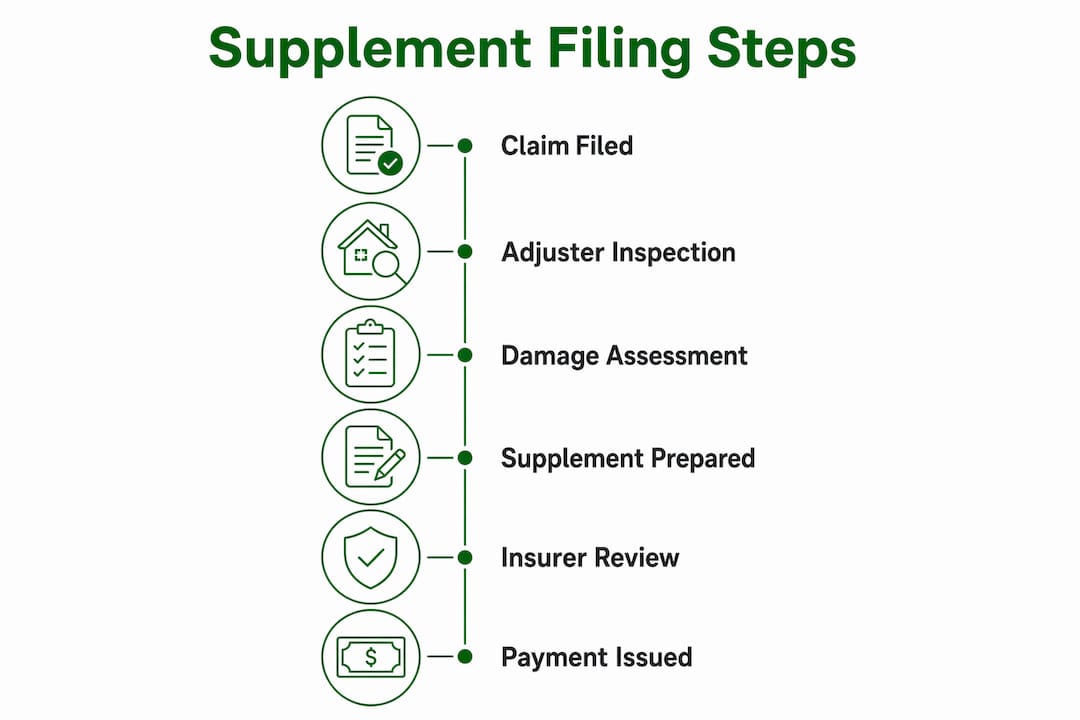

A storm damage supplement is a second, formal submission to your insurance carrier that requests payment for damage items missed or underpriced in the original claim scope. It is not a dispute or an appeal of a denied claim. A supplement addresses missed damage discovered after the initial inspection, which is a critical distinction every homeowner needs to understand.

The process starts when an insurance adjuster visits your property and creates a scope of loss. That scope lists every damaged item and assigns a cost to each one. Adjusters work quickly and often miss secondary damage, code upgrade requirements, or items that only become visible once repairs begin. When your contractor identifies those gaps, a supplement is the correct tool to address them.

Common triggers for a supplement include missed shingle damage, underestimated quantities of materials, required building code upgrades, and permit costs. Each of these is a legitimate, documentable line item. State laws require insurance carriers to respond within 30–90 days after receiving a complete supplemental submission.

Pro Tip: Ask your contractor to walk the roof with you before signing any repair contract. A second set of trained eyes catches damage the adjuster may have missed, which strengthens your supplement before you even file it.

A licensed contractor or a public adjuster typically prepares the supplement on your behalf. They compare the insurer's scope line by line against the actual repair estimate. That comparison becomes the foundation of the submission, along with photos, permits, and written explanations for each added item.

Why storm damage supplements matter for your wallet

Supplements produce a measurable financial difference. Supplements average a 34.4% increase in RCV payouts on residential claims. That figure reflects how consistently initial estimates fall short of actual repair costs.

The dollar impact is equally clear. Skipping a supplement can leave $1,500 to $8,000 per claim unclaimed. For property managers overseeing multiple buildings, that gap multiplies across every storm-affected asset.

Supplements also cover costs that homeowners rarely think to claim on their own:

- Code compliance upgrades: Local building codes change over time. Repairs must meet current standards, and the cost difference is a legitimate supplement item.

- Overlooked secondary damage: Gutters, fascia, and underlayment are frequently missed in the initial scope.

- Permit and inspection fees: These are real costs tied directly to the repair and belong in the claim.

- Disposal and haul-away costs: Removing old roofing materials carries a cost that adjusters sometimes exclude.

Insurers expect supplements as a routine, legitimate claim phase rather than signs of a dispute. Filing one does not flag your account or put you at risk of cancellation. It is simply the second step in a two-step process that the industry treats as standard.

Common challenges and misconceptions about supplements

The biggest misconception homeowners carry is that filing a supplement means fighting with their insurer. That framing creates unnecessary stress. Carriers treat initial settlements as opening positions, and supplements are the expected mechanism for correcting them.

A second common mistake is submitting a supplement verbally or without detailed documentation. A phone call to your adjuster does not constitute a supplement. The submission must be written, itemized, and supported by evidence. Without that structure, carriers have no obligation to act on your request.

Timing is a third pitfall. Delayed filing beyond 30–60 days increases denial rates because carriers can argue the additional damage occurred after the storm. Filing promptly after the initial claim closes that argument before it opens.

Pro Tip: Keep a written log of every conversation with your insurance carrier, including the date, the name of the representative, and a summary of what was discussed. That record protects you if the carrier later disputes the timeline.

One serious risk deserves a direct warning. Assignment of Benefits agreements can strip you of control over your own claim. Some contractors ask homeowners to sign an AOB, which transfers claim rights to the contractor. Once signed, you lose the ability to negotiate, approve, or reject settlement terms. Avoid signing any AOB without consulting a licensed public adjuster or attorney first.

How to prepare and submit an effective supplement

A well-prepared supplement follows a clear sequence. Each step builds the evidence the carrier needs to approve the additional payment.

- Get a detailed contractor estimate. The estimate must list every repair item with individual quantities and unit costs. Vague totals do not hold up in a supplement review.

- Compare the estimate to the insurer's scope line by line. Identify every item the carrier included, every item it missed, and every item it underpriced. This comparison is the core of your supplement.

- Use estimating software output when possible. Line-by-line scope comparison using Xactimate is the industry standard for credible supplements. Carriers recognize Xactimate reports and process them faster than informal estimates.

- Photograph every item in the supplement. Photos must show the specific damage tied to each line item. General roof photos are not enough. Learn the right approach to document storm roof damage before you start shooting.

- Include permits and code documentation. If local codes require upgraded materials or additional work, attach the relevant code sections and permit requirements to the submission.

- Write a clear explanation for each added item. One or two sentences per item is enough. Explain what was missed, why it is storm-related, and what it costs.

- Submit in writing, referencing your original claim number. Email creates a timestamp. Send everything to your adjuster and copy the carrier's claims department directly.

- Follow up in writing at the 30-day mark. If you have not received a response, send a written follow-up and document that you did so.

For a broader view of the full claims process, the storm damage claim process guide from Chattanoogaroofrepairs walks through each stage from initial inspection to final payment. The storm damage workflow guide from Thomas Roofing also provides a useful step-by-step framework from the homeowner's perspective.

Properly prepared supplements with clear documentation greatly increase approval rates. The documentation is not a formality. It is the argument.

Key Takeaways

A storm damage supplement is the standard second step in any insurance claim where the initial estimate fails to cover the full cost of repairs.

| Point | Details |

|---|---|

| Supplements are not disputes | They address missed or underpriced damage, not denied claims. |

| Financial impact is significant | Skipping a supplement can leave $1,500 to $8,000 per claim unclaimed. |

| Timing matters | File within 30–60 days of the initial claim to reduce denial risk. |

| Documentation drives approval | Line-by-line estimates, photos, and written justifications are required. |

| AOB agreements carry real risk | Signing one transfers your claim rights to the contractor. |

Why I tell every homeowner to expect a supplement

After years of watching homeowners navigate storm claims, the pattern is consistent. The first check from the insurance company is almost never the last one. Adjusters are not trying to shortchange you. They are working fast, often in difficult conditions, and they cannot see damage that is hidden under shingles or inside gutters.

The homeowners who recover the full cost of their repairs are the ones who treat the supplement as a planned step, not a surprise. They hire a contractor who documents everything, they file promptly, and they stay in written communication with their carrier throughout. The ones who struggle are the ones who accept the first estimate and assume it is final.

My honest advice is this: before you sign a repair contract, ask the contractor whether they have experience preparing supplemental claims. A contractor who knows how to read an insurance scope and identify gaps is worth far more than one who simply replaces shingles. The supplement process is where real money is either recovered or lost.

The stress homeowners feel around supplements usually comes from not knowing what to expect. Once you understand that insurers expect this process and that it is a normal part of every significant storm claim, the anxiety disappears. You are not asking for anything extra. You are asking for what the policy already covers.

— Steve

Chattanoogaroofrepairs is ready to help with your storm claim

Storm damage repairs move fast, and the documentation window closes faster than most homeowners realize. Chattanoogaroofrepairs provides thorough 21-point inspections that capture every item of damage before the adjuster's estimate becomes final.

Our team works with GAF and Owens Corning materials and carries full licensing and insurance throughout Chattanooga and the surrounding area. We prepare detailed contractor estimates that align with Xactimate standards, giving your supplement the credibility it needs for approval. Whether you need metal roofing repair or a full roofing service assessment, we provide transparent pricing and no-pressure consultations. Contact Chattanoogaroofrepairs today for a free inspection and let us help you recover the full value of your claim.

FAQ

What is a storm damage supplement in simple terms?

A storm damage supplement is a formal written request to your insurance company for additional payment when the original claim estimate missed damage or underpriced repairs. It is a standard part of the claims process, not a dispute.

How much more money can a supplement recover?

Supplements average a 34.4% increase in Replacement Cost Value payouts on residential claims. Homeowners who skip the process can leave $1,500 to $8,000 per claim unclaimed.

How long does the insurer have to respond to a supplement?

State laws generally require insurance carriers to respond and settle supplemental claims within 30–90 days of receiving complete documentation.

When should I file a storm damage supplement?

File as soon as your contractor identifies missed or underpriced damage, ideally within 30–60 days of the initial claim. Delayed filing increases the risk that the carrier will argue the additional damage is unrelated to the original storm.

Can my contractor file a supplement on my behalf?

Yes. A licensed contractor or public adjuster can prepare and submit a supplement using your original claim number. Avoid signing an Assignment of Benefits agreement, which transfers your claim rights to the contractor and removes your ability to approve settlement terms.