A roofing material upgrade is defined as any modification during repair or replacement that improves your roof beyond its original condition, using better materials or components than what was first installed. This covers everything from synthetic underlayment and Class 4 impact-resistant shingles to advanced metal flashing and UV-silicone pipe boots. Understanding what is a roofing material upgrade matters because the choice affects your insurance premiums, resale value, and long-term maintenance costs. Most homeowners don't realize that insurance typically covers only like-kind replacement, meaning upgrades come out of pocket unless you negotiate otherwise.

What is a roofing material upgrade and what types are available?

A roofing material upgrade goes beyond swapping old shingles for identical new ones. The industry term for this category of work is a "betterment," meaning you are improving the roof's performance or durability beyond its pre-loss or pre-replacement condition. Upgrades are optional and are not covered by standard homeowners insurance, which pays only for like-kind replacement. That distinction matters before you budget.

The most common upgrade options fall into these categories:

- Class 3 and Class 4 impact-resistant shingles. These carry an UL 2218 rating and resist hail damage far better than standard three-tab or architectural shingles. Class 4 is the highest rating and qualifies for insurance discounts in most hail-prone states. Learn more about shingle durability factors before choosing a product.

- Synthetic underlayment. Standard felt paper tears and absorbs moisture. Synthetic underlayment resists tearing, repels water, and lasts longer under the surface shingles.

- Metal roofing and standing seam panels. Metal roofs carry lifespans of 40–70 years and reflect solar heat. Standing seam panels eliminate exposed fasteners, reducing leak points significantly.

- Advanced flashing techniques. W-valley flashing and step flashing with sealant tape outperform basic open-valley methods. Flashing failures cause a large share of residential roof leaks.

- Upgraded pipe flashing. Standard rubber pipe boots wear out 10–15 years before the roof itself. UV-silicone pipe flashings reduce leaks and eliminate a common maintenance headache.

- Drip edge metal flashing. This low-cost addition, typically $150–$400, directs water away from fascia boards and prevents rot. Many contractors skip it unless you ask.

- Cool roofing materials. Reflective shingles and coatings meet ENERGY STAR standards and reduce attic heat buildup. They pair well with upgraded ridge ventilation for maximum airflow.

Pro Tip: Ask your contractor specifically about drip edge and pipe boot upgrades during any full replacement. These two items cost little at installation time but prevent expensive repairs later.

How do roofing upgrades affect your home's value and insurance costs?

The financial case for upgrading roofing materials is stronger than most homeowners expect. Standard roof replacement recovers 56–72% of its cost at resale, but Class 4 impact-resistant shingles or metal roofs can deliver ROI of 60–120% when insurance discounts and maintenance savings are factored in. That range reflects the full picture, not just the sale price bump.

Insurance premium savings

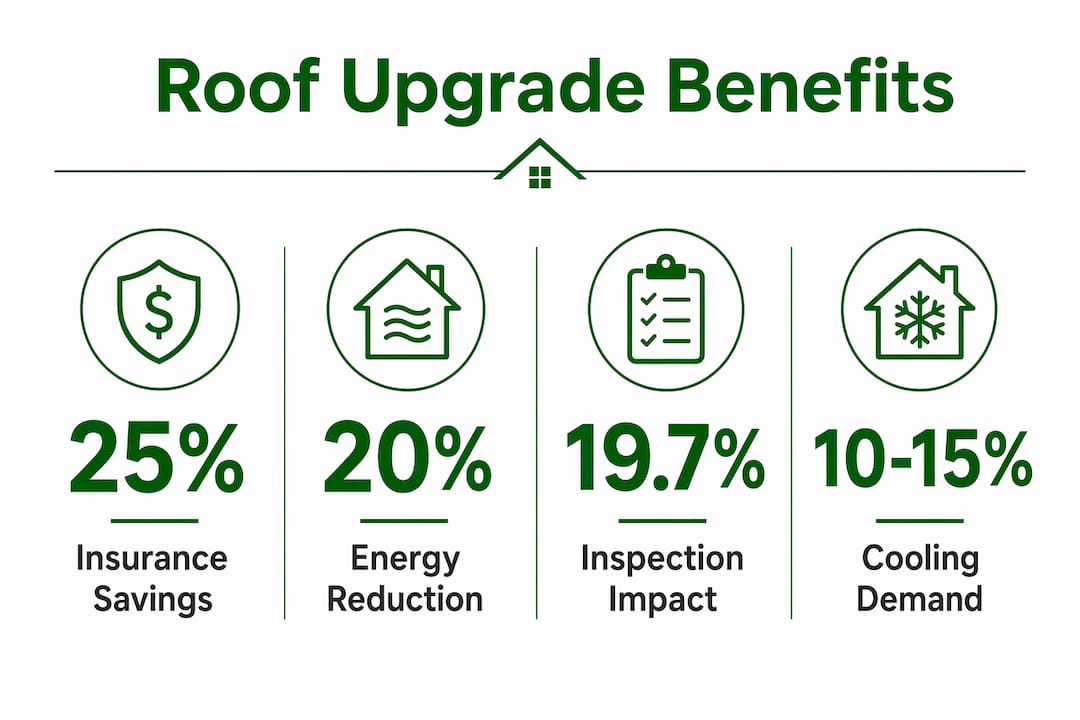

Class 4 impact-resistant shingles generate insurance discounts of 10–25% annually, and in hail-prone regions like Tennessee, those discounts can run even higher. At that rate, the premium savings alone often pay for the upgrade within 6–12 years. After you install qualifying shingles, request a certificate of completion and submit it to your insurer. That document triggers a formal premium reassessment. Without it, you may wait months or never see the discount applied.

Resale value and inspection protection

Roof condition is the second-leading deal-killer in home inspections, responsible for 19.7% of failures. Buyers routinely demand $8,000–$12,000 in credits when inspectors flag roof issues. An upgraded roof eliminates that negotiating leverage entirely. For a $450,000 home, high-quality roofing upgrades can add $13,500–$22,500 in value, a 3–5% increase. That figure reflects both the direct value and the avoided buyer credits.

Energy savings from cool roofing

Cool roofing materials reduce peak cooling energy demand by 10–15%. In Chattanooga's hot summers, that reduction translates to meaningful monthly savings on electricity bills. Over a 20-year roof lifespan, those savings compound and lower the effective net cost of the upgrade. Homeowners in hot climates see the fastest payback from this category.

The right way to evaluate any upgrade is through net cost over the roof's full lifespan. When you add insurance savings, energy reductions, and avoided premature replacement cycles together, premium roofing materials often cost less than standard options over 20 years despite the higher upfront price. That is the calculation worth running before you decide.

When should you decide to upgrade your roofing materials?

Timing a roofing upgrade correctly saves money and avoids paying for work twice. The right moment to upgrade is during a full replacement, not a patch repair. Adding synthetic underlayment or Class 4 shingles to a partial repair is rarely practical or cost-effective.

Use these criteria to decide whether an upgrade makes sense for your home:

- Your roof is 15 or more years old. At this age, standard shingles are past their midpoint. Replacing them with upgraded materials resets the clock and adds decades of protection.

- You live in a high-risk climate zone. Chattanooga and surrounding areas face hail, wind, and heavy rain. Impact-resistant shingles and metal roofing are built for exactly these conditions.

- You plan to sell within 5–10 years. Upgraded materials improve inspection outcomes and reduce buyer credits, as noted above. The resale timing matters for calculating your return.

- Your insurer offers Class 4 discounts. Call your insurance agent before signing a roofing contract. Confirm which products qualify for premium reductions and get that in writing.

- Your current roof has recurring leak points. If the same areas fail repeatedly, a material upgrade addresses the root cause rather than patching symptoms.

Pro Tip: Before your contractor starts work, check whether your local building code requires any upgrades, such as drip edge or ice-and-water shield. Code-required changes are different from optional upgrades, and your insurer may handle them differently.

Professional installation is not optional when it comes to upgrades. Proper installation of the full roofing system matters as much as the material itself. A Class 4 shingle installed incorrectly will fail early and void the manufacturer warranty. Chattanoogaroofrepairs uses certified installation methods and works with GAF and Owens Corning materials to protect both the product warranty and your investment.

One overlooked factor is insurance claim compliance. If storm damage triggers your replacement, document every upgrade you choose separately from the insurance-covered scope. Insurers pay for like-kind replacement. Upgrades are your responsibility to fund, but they also generate the discounts and value gains described above. Keeping that paperwork clean prevents disputes later.

What are the common pitfalls and misconceptions about roofing upgrades?

Several widespread beliefs about roofing upgrades lead homeowners to make poor decisions or spend money in the wrong places.

- "My insurance will cover the upgrade." Standard homeowners insurance covers like-kind replacement only. Upgrades are out-of-pocket expenses unless your policy includes an extended replacement cost endorsement. Review your roofing insurance coverage before assuming otherwise.

- "Expensive material equals a better roof." Material quality matters, but installation quality matters equally. A premium shingle installed without proper underlayment, flashing, or ventilation will underperform a mid-grade shingle installed correctly. The whole system has to work together.

- "Code-required changes are the same as upgrades." They are not. Building codes sometimes require improvements over original materials, such as adding ice-and-water shield in certain climate zones. Insurers may apply a betterment deduction to code-driven changes, treating them differently from voluntary upgrades. Understanding that distinction helps you negotiate your claim correctly.

- "More features always mean better ROI." Some upgrades deliver clear payback. Others, like decorative ridge caps or premium color blends, add cost without measurable financial return. Prioritize upgrades that address failure points, such as flashing, pipe boots, and underlayment, before spending on aesthetics.

- "The surface shingles are all that matter." The roofing surface is only one layer of a system that includes underlayment, decking, flashing, ventilation, and gutters. Upgrading shingles while leaving worn flashing or inadequate ventilation in place limits the benefit of the better material.

Upgrading your roof's full system rather than just the surface shingles is the approach that delivers lasting results. Homeowners who focus only on the visible layer often find themselves dealing with leaks from flashing or ventilation failures within a few years of a costly replacement.

Key Takeaways

A roofing material upgrade delivers the most value when it addresses the full roof system, not just the surface, and when insurance savings and energy efficiency are factored into the total cost calculation.

| Point | Details |

|---|---|

| Upgrades are out-of-pocket costs | Insurance covers like-kind replacement only; upgrades require separate budgeting. |

| Class 4 shingles cut insurance costs | Annual premium discounts of 10–25% often recover upgrade costs within 6–12 years. |

| Cool roofing reduces energy bills | Reflective materials cut peak cooling demand by 10–15%, lowering net costs over time. |

| Full system quality beats material alone | Proper installation of underlayment, flashing, and ventilation matters as much as shingle grade. |

| Roof condition protects resale value | Upgraded roofs prevent $8,000–$12,000 in buyer credits during home sale inspections. |

Why I think most homeowners underestimate the upgrade decision

After years of watching homeowners navigate roofing projects, the pattern I see most often is this: people focus almost entirely on the shingle brand and color, then sign off on whatever underlayment and flashing the contractor defaults to. That is exactly backwards.

The shingle is the most visible part of your roof, but it is rarely where roofs fail first. Pipe boots, valley flashing, and underlayment fail years before the shingles show wear. Upgrading those components costs a fraction of the shingle upgrade and prevents the leaks that cause real damage inside your home.

The other mistake I see is treating the upgrade decision as a pure upfront cost question. The homeowners who come out ahead are the ones who run the full 20-year math: insurance discounts, energy savings, avoided repairs, and resale protection. When you account for all of that, a Class 4 shingle or a metal roof often costs less than a standard replacement over its full life. That is not a marketing claim. It is arithmetic.

My practical advice: before you sign any roofing contract, call your insurance agent and ask which materials qualify for premium discounts in your zip code. Get that answer in writing. Then ask your contractor to price the upgrade separately so you can see the exact delta. Most homeowners are surprised by how small the gap is between standard and upgraded materials when the insurance math is applied.

— Steve

Chattanoogaroofrepairs can help you upgrade the right way

Choosing the right upgrade is one decision. Getting it installed correctly is another. Chattanoogaroofrepairs works with homeowners across Chattanooga and surrounding areas to plan and execute roofing replacements using GAF and Owens Corning materials, including Class 4 impact-resistant shingles and full metal roofing systems.

If you are considering a metal roof, Chattanoogaroofrepairs offers metal roofing in Chattanooga with certified installation and manufacturer-backed warranties. For homeowners weighing shingle upgrades, the shingle replacement service covers impact-resistant options with transparent pricing and no-pressure consultations. Contact Chattanoogaroofrepairs to get a clear cost estimate and upgrade recommendation based on your home's specific needs.

FAQ

What is a roofing material upgrade exactly?

A roofing material upgrade is any improvement during repair or replacement that exceeds the roof's original condition, such as switching from standard shingles to Class 4 impact-resistant shingles or adding synthetic underlayment. It is distinct from a like-kind replacement, which restores the roof to its prior state.

Does homeowners insurance pay for roofing upgrades?

Standard homeowners insurance covers only like-kind replacement and does not pay for upgrades. Upgrades are the homeowner's responsibility, though they often generate insurance premium discounts that recover the cost over time.

Which roofing upgrade offers the best return on investment?

Class 4 impact-resistant shingles and metal roofing offer the strongest combined ROI when insurance discounts of 10–25% annually and energy savings are included alongside resale value gains. The payback period for Class 4 shingles is typically 6–12 years through premium reductions alone.

What is the most overlooked roofing upgrade?

Drip edge metal flashing is one of the most overlooked upgrades. It costs $150–$400 during a full replacement but prevents thousands of dollars in fascia rot and water damage over the roof's life.

How does cool roofing reduce energy costs?

Cool roofing materials reflect solar heat and reduce peak cooling demand by 10–15%, which lowers monthly electricity bills. The savings are most significant in hot climates and compound over the roof's full lifespan.